Carbon Finance for NbS in Southeast Asia: Costs and Investment Opportunities in 5 Key Countries

Background

Nature-based Solutions (NbS) are increasingly valued in the global carbon market as cost-effective climate change mitigation measures, supporting livelihoods, biodiversity and climate change adaptation. In 2024, an estimated 37 million NbS credits were transacted, accounting for 43.8% of voluntary market trading volume [1]. Compliance markets such as Singapore’s carbon tax and CORSIA are also opening to NbS credits, expanding potential demand. Singapore’s recent Request for Proposal to procure NbS credits further reinforces institutional demand.

Building on this momentum, this report examines NbS carbon credit supply and cost potential in Indonesia, Malaysia, Thailand, Cambodia, and the Philippines—countries accounting for over 99.5% of Southeast Asia’s issuance of such credits and representing the region’s diverse and evolving NbS landscape.

In Southeast Asia, terrestrial forests were lost at a rate of 0.59% annually, with 1.45 million hectares lost from 2000 to 2010 [2], and mangrove forests were also depleted at an average rate of 0.18% annually, with over 100,000 hectares removed from 2000 to 2012 [3]. These losses underscore both the urgency and opportunity for restoration, with the region’s carbon-rich tropical climate enhancing its suitability for NbS projects [4]. Across Southeast Asia, 121 million hectares of terrestrial reforestation potential (~3.4 GtCO₂e/yr) [4] and 0.5 million hectares of mangrove restoration potential (~0.2 GtCO₂e/yr) [5] highlight the region’s strong long-term NbS prospects.

Terrestrial and coastal forest restoration are not only high-potential solutions but also market-preferred, yet their current supply remains limited, leaving considerable room for growth [6, 7]. This analysis assesses their cost and sequestration performance to identify early-stage investment opportunities in tropical terrestrial forests and coastal mangroves.

Cost and Market Dynamics of Reforestation and Blue Carbon NbS

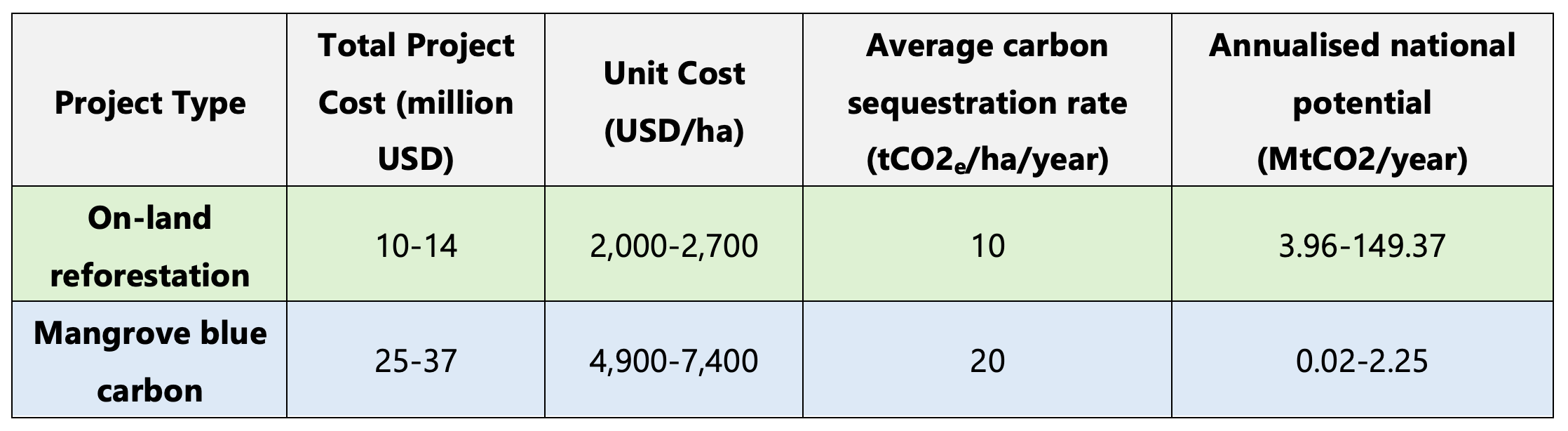

Table 1 - Comparative overview of indicative cost and mitigation metrics for on-land and mangrove-based NbS projects across 5 countries

The total project cost range (10-37 million USD) reflects typical total investment requirements per project, modeled for a 5,000-hectare, 40-year implementation across five study countries in Southeast Asia, while unit costs (USD 2,000-7,400/ha) represent average project-level expenditures. The average carbon sequestration rates of 10 and 20 tCO₂ per hectare per year are modeled assumptions consistent with published estimates for tropical reforestation and mangrove systems [8] in Southeast Asia.

The broad national potential ranges (3.96-149.37 MtCO₂/year for on-land reforestation and 0.02-2.25 MtCO₂/year for mangroves) illustrate the variation in biophysical and land availability conditions among countries. Together, these figures highlight the trade-offs between cost, efficiency, and scalability across different NbS pathways.

While both on-land reforestation (terrestrial forest) and blue carbon (coastal mangrove forest) projects offer strong mitigation potential, their cost structures, scalability, and geographical constraints differ. On-land reforestation generally requires lower investment per hectare (2,000-2700 USD/ha) making it more feasible in resource-constrained contexts, while mangrove restoration is often higher (4,900-7,400 USD/ha) affected by site-specific hydrology, ecological engineering needs, and elevated failure risks [9].

Despite these differences, both remain underrepresented in Southeast Asia’s carbon market. In Indonesia, on-land reforestation projects are listed but have not yet issued credits despite an estimated 149 MtCO₂ per year potential; in the Philippines, the MinTrees project has delivered 12,685 credits despite a national 36 million tCO₂/year potential. For mangrove restoration, Indonesia’s 2.25 million tCO₂/year potential contrasts with the 397,071 credits issued to date. These wide gaps between issuance and potential illustrate the underrepresentation of NbS pathways and highlight the significant scope for scaling them up.

Unlocking NbS Potential in Southeast Asia: Country-Level Insights

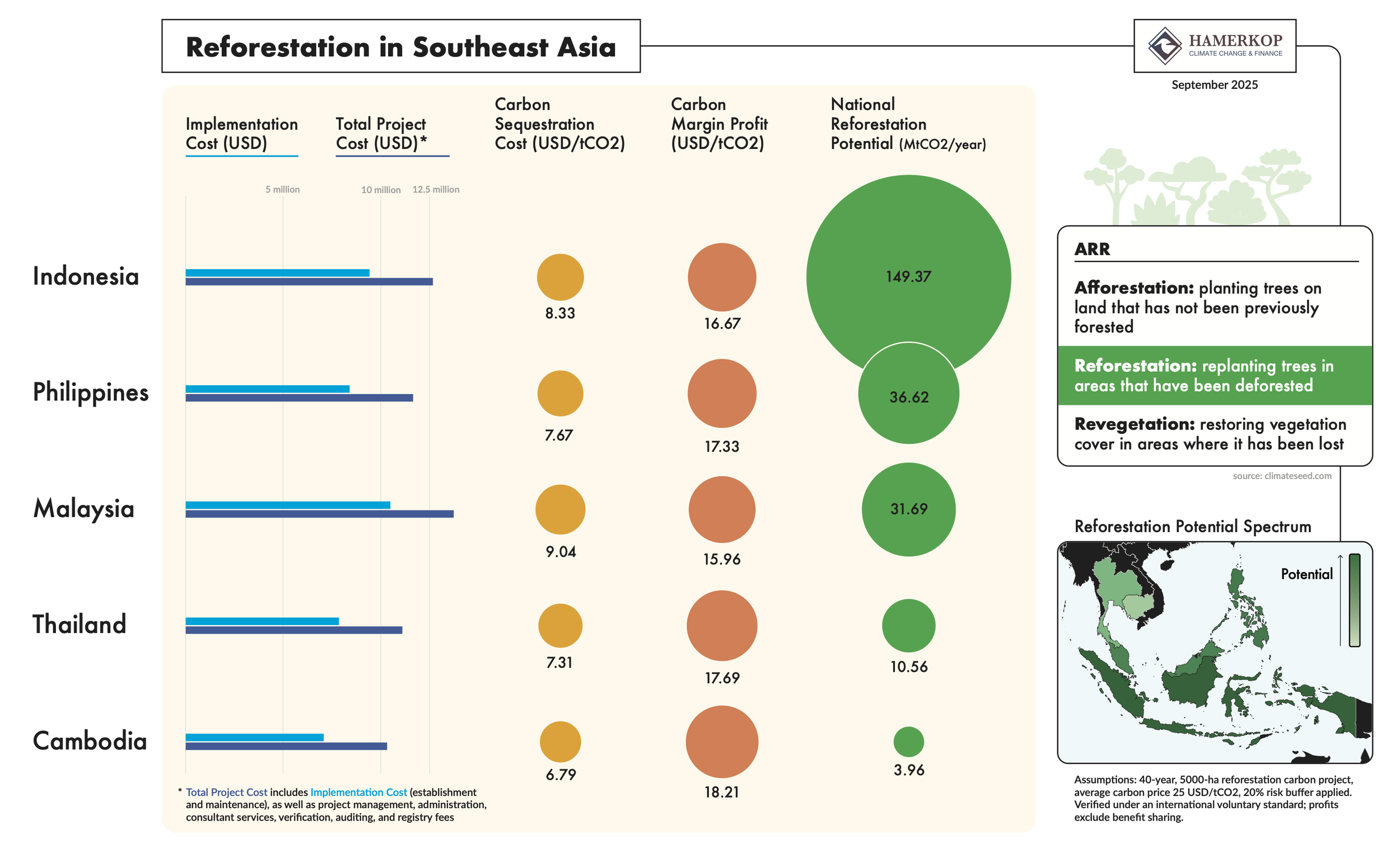

Figure 1 - Comparative costs, carbon efficiency, and national potential of reforestation projects in Southeast Asia.

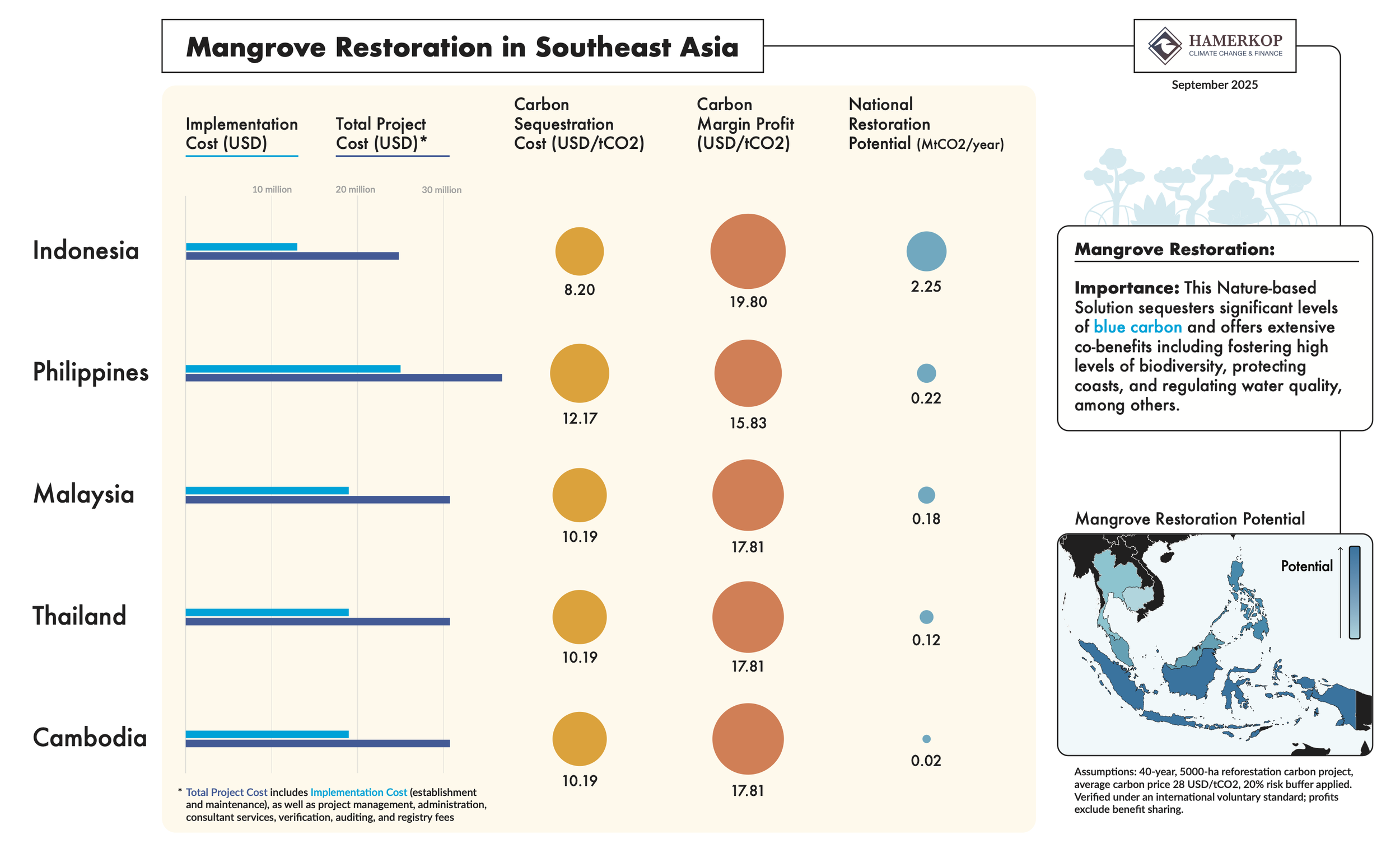

Figure 2 - Comparative costs, carbon efficiency, and national potential of mangrove restoration projects in Southeast Asia.

Detailed assumptions on cost structure, project scale, and carbon price modeling are provided in the Methodology and Modelling Assumptions section below. As in figures above, reforestation and blue carbon projects exhibit wide variation in costs, returns, and mitigation potential across countries. These differences are not only technical but also interact with broader market and policy conditions, where stable policy frameworks, credible registries, and institutional capacity will ultimately shape how such potential can be translated into actual supply and opportunities realized.

Indonesia

Indonesia combines mature NbS systems with high removal potential: 149 MtCO₂/year from on-land reforestation and 2.25 MtCO₂/year from mangroves restoration. It leads the region in international-standard credit issuance, driven by REDD+ and mangrove restoration, and is expanding into ARR (Afforestation, Reforestation, and Revegetation). This is underpinned by a slightly more mature ecosystem, a domestic system (i.e., Sistem Registri Nasional), and positive market uptake from corporate buyers. Stronger registry flexibility and Mutual Recognition Agreements (MRAs) with international standards including Verra, which enables cross-recognition of verified credits, would further boost transactions.

Philippines

The Philippines has limited reforestation experience through the MinTrees project, which has issued the first batch of ARR credits in the country with a high market uptake (e.g., 78.5% retirement rate by April 2025). With moderate on-land reforestation average carbon abatement costs (USD 7.67/tCO₂), it has two registered and three developing projects. The country is gearing up to realise its 36.62 MtCO₂/year reforestation potential. The NBCAP (National Blue Carbon Action Project) targets 5,000 ha of mangrove restoration and explores JCM (Joint Crediting Mechanism) credits with Japan [10].

Thailand

Thailand’s NbS activity remains domestically focused under the T-VER (Thailand Voluntary Emission Reduction) program, which has issued 587,000 forestry and agriculture credits. Ongoing projects are expected to issue 1.23 million tCO₂ per year, but the absence of international registry linkages limits buyer diversity. Closer alignment with international standards could expand buyer access and market potential.

Malaysia

Malaysia is exploring mangrove restoration alongside its past Improved Forest Management (IFM) experience. Institutional capacity is growing, with the Bursa Carbon Exchange operational and a domestic market-based crediting framework (e.g. Forest Carbon Offset) under development. Blue carbon project development is emerging through stakeholder engagement for a Sarawak Mangrove Restoration [11], contributing to Malaysia’s broader blue carbon annual mitigation potential of 180,000 tCO₂.

Cambodia

Cambodia’s current issuance is REDD+ focused, with one mangrove project under development. While on-land reforestation annual potential is limited to 3.96 million tCO₂, it has the lowest reforestation cost (USD 2,066 per ha) among the five countries, offering value for cost-sensitive investors. Stronger policies and registry systems would enhance market confidence.

Methodology and Modelling Assumptions

The costs of NbS projects assessed in this study fall into five key categories: pre-implementation costs (site selection, feasibility studies, PDD preparation), implementation costs (planting, fencing, seedling supply, infrastructure), management costs (coordination, administration, carbon asset management, consultations), MRV costs (field measurements, remote sensing, verification), and transaction and certification costs (validation, registry fees, insurance). The cost assessment takes into consideration the full project life cycle and recognises that expenses are not evenly distributed over time.

Data on project costs, carbon sequestration rates, and mitigation potential were compiled from Verra-registered PDDs, peer-reviewed studies, and industry reports. The dataset was screened for quality and comparability, and was used to parameterise a cost-modelling framework for project- and country-level estimation. Key assumptions were refined through expert consultation to ensure consistency and realism.

In modelling, both on-land reforestation and individual mangrove restoration projects were assumed to cover a total area of 5,000 ha over a 40-year crediting period under a 7% discount rate. For Reforestation, the project used active forest plantation with a sequestration rate of 10 tCO₂/ha/year and a carbon price of 25 USD/credit (reflecting risk buffer deductions). For mangrove restoration, the project followed an active planting–based reforestation with a sequestration rate of 20 tCO₂/ha/year and a carbon price of 28 USD/credit (reflecting risk buffer deductions).

References:

[1] Ecosystem Marketplace, State of the voluntary carbon market 2025, F.T. Association., Editor. 2025.

[2] Stibig, H.-J., et al., Change in tropical forest cover of Southeast Asia from 1990 to 2010. Biogeosciences, 2014. 11(2): p. 247-258.

[3] Richards, D.R. and D.A. Friess, Rates and drivers of mangrove deforestation in Southeast Asia, 2000–2012. Proceedings of the National Academy of Sciences, 2016. 113(2): p. 344-349.

[4] Zeng, Y., et al., Economic and social constraints on reforestation for climate mitigation in Southeast Asia. Nature Climate Change, 2020. 10(9): p. 842-844.

[5] Alliance, G.M., The State of the World’s Mangroves 2024. 2024, Global Mangrove Alliance.

[6] Friess, D.A., et al., Capitalizing on the global financial interest in blue carbon. PLoS Climate, 2022. 1(8): p. e0000061.

[7] S, S. ARR Carbon Credits: The Next Gold Rush Backed by Google and Microsoft. 2025; Available from: https://carboncredits.com/arr-carbon-credits-the-next-gold-rush-backed-by-google-and-microsoft/.

[8] Jiang, Y., et al., Restoring mangroves lost by aquaculture offers large blue carbon benefits. One Earth, 2025. 8(1).

[9] Bayraktarov, E., et al., The cost and feasibility of marine coastal restoration. Ecological applications, 2016. 26(4): p. 1055-1074.

[10] World Economic Forum. The Philippines kicks-off pioneering National Blue Carbon Action Partnership. 2025; Available from: https://www.weforum.org/friends-of-ocean-action/the-philippines-kicks-off-pioneering-national-blue-carbon-action-partnership/#:~:text=The%20Philippines%20first%20announced%20joining,both%20people%20and%20the%20planet).

[11] Borneo Post. Sarawak launches first Blue Carbon Project in Tanjung Manis to restore 10,232 ha of mangroves. 2025; Available from: https://www.theborneopost.com/2025/03/20/sarawak-launches-first-blue-carbon-project-in-tanjung-manis-to-restore-10232-ha-of-mangroves/.